Get free Consultant With out Experts.

Notice: File your Company Audit before the 30th September deadline. Talk to our expert

India’s highest-rated

legal tax and compliance platform.

Talk to our experts to kickstart your business registration process.

Tax collected by the seller from the buyer on sale so that it can be deposited with the tax authorities. Section 206C of the Income-tax Act governs the goods on which the seller has to collect tax from the buyers.

Tax Collected at Source (TCS) refers to the tax collected by the seller or collector of certain goods or services from the buyer at the point of sale. This mechanism is similar to TDS (Tax Deducted at Source), but in the case of TCS, the tax is collected instead of deducted. The seller is responsible for collecting this tax and remitting it to the government.

TCS is applicable on certain transactions specified under the Income Tax Act, such as the sale of specific goods (e.g., scrap, timber, coal), foreign remittance, and cash withdrawals above a prescribed limit. The rates of TCS depend on the type of goods or services and can vary.

To comply with tax regulations, businesses or entities that collect TCS are required to file TCS returns periodically. These returns provide details of the amount of tax collected, the buyer’s details, and the payment to the government. The return is typically filed quarterly using Form 27EQ, and the due dates for filing vary depending on the quarter. Failure to file TCS returns on time can result in penalties, so businesses must ensure accurate reporting and timely submission to avoid fines or interest.

The legal liability of a private limited company's stockholders is restricted. You will be responsible for paying the liabilities of the company as a shareholder to the extent of your contribution. This protects your personal assets to cover the company's debts.

By collecting taxes at the point of sale, TCS helps ensure that taxes are collected in advance, improving the efficiency of government revenue collection.

As the tax is collected by the seller and directly deposited with the government, the chances of tax evasion are reduced, leading to greater transparency in business transactions.

Buyers who have TCS collected on their purchases can claim it as a tax credit when filing their Income Tax Returns, which can be adjusted against their total tax liability.

TCS simplifies the process for tax authorities by automatically collecting taxes at the point of transaction, reducing the burden of following up with individual taxpayers.

TCS applies to high-value transactions, ensuring that businesses or individuals engaging in substantial dealings contribute to the tax system without delay.

Eligibility Criteria for TCS (Tax Collected at Source)

Seller’s Obligation:

TCS is applicable to sellers or collectors who are involved in specific transactions, such as the sale of goods (e.g., scrap, timber) or services (e.g., travel packages).

Transaction Type:

TCS applies to high-value transactions like the sale of specified goods, cash withdrawals above a prescribed limit, and foreign remittance.

Threshold Limits:

Sellers or collectors must ensure their sales or transactions exceed the prescribed limits for TCS to apply, as defined under the Income Tax Act.

Business Entity:

Typically, businesses or entities involved in regular trade or commerce are required to collect TCS, with some exceptions.

TCS (Tax Collected at Source) Filing Checklist

TCS Collection Details:

TCS Amount:

Buyer Information:

Form 27EQ:

Payment Receipts:

Due Dates:

Tax Credit:

Documents Required for TCS Filing

TCS Collection Records:

Buyer’s Information:

Form 27EQ:

Payment Proof:

Tax Credit Certificates:

Alcoholic Liquor for Human Consumption: 1% Tendu Leaves: 5% Timber obtained under a forest lease: 2.5% Timber obtained by any mode other than forest lease: 2.5% Any other forest produce (excluding timber and tendu leaves): 2%

Motor Vehicles (Exceeding ₹10 Lakhs): 1%

Foreign Remittance under Liberalized Remittance Scheme (LRS) 5% on amounts exceeding ₹7 lakhs in a financial year. 10% if PAN/Aadhaar is not provided.

Applicable on Sale of Goods exceeding ₹50 Lakhs by the Seller TCS Rate: 0.1% 1% if PAN/Aadhaar is not provided. Exclusions Goods already subject to other TCS provisions or GST.

Higher TCS Rates If the buyer has not filed their income tax return for the last two years and the TDS/TCS exceeds ₹50,000 in each year, the TCS rate is higher of Twice the specified TCS rate, or 5%.

Here are the key characteristics of Tax Collected at Source (TCS):

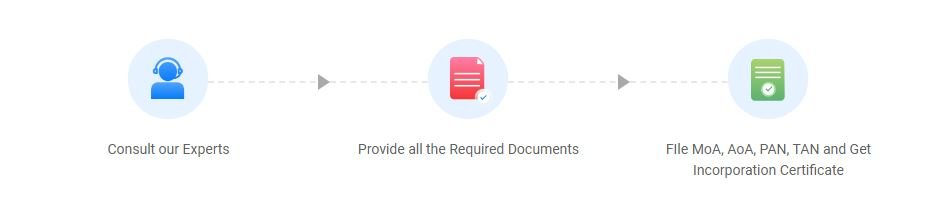

If you’re required to collect and deposit TCS under the Income Tax Act, follow these steps to register for TCS:

Let me know if you need further assistance with any step!

At ADTAXS, we are committed to providing expert consulting services to help your business succeed. Our specialties include comprehensive tax solutions, legal advisory, and essential business registration.

By continuing past this page, you agree to our Terms and conditions , Cookie Policy, Privacy Policy and Refund Policy © – DAV Business Services Pvt. Ltd. All rights reserved.

Copyright © 2010-2024, All Right Reserved DAV Business Services Pvt. Ltd.