Get free Consultant With out Experts.

Notice: File your Company Audit before the 30th September deadline. Talk to our expert

India’s highest-rated

legal tax and compliance platform.

Talk to our experts to kickstart your business registration process.

The Companies Act, 2008 governs companies in India, but it does not directly apply to LLPs. LLPs are regulated separately under the Limited Liability Partnership Act, 2008, which defines the incorporation process, rights, and responsibilities of partners.

A Limited Liability Partnership (LLP) is a business structure that blends the benefits of a partnership with the protections typically offered by a corporation. In an LLP, the partners enjoy limited liability, meaning they are not personally liable for the business’s debts or liabilities beyond their investment, protecting their personal assets. This structure is ideal for professional service firms, such as law firms or accounting firms, where partners need flexibility in management but want to shield themselves from the liabilities caused by the actions of other partners. LLPs also benefit from pass-through taxation, where profits and losses are reported on the partners’ individual tax returns, avoiding the issue of double taxation. Additionally, LLPs provide flexibility in their internal operations, allowing partners to manage the business without the rigid structure of a corporation. This makes LLPs an attractive option for those seeking a balanced approach between liability protection and operational flexibility.

Partners’ liability is restricted to their agreed capital contribution.

LLP exists independently, distinct from its partners legally.

Compliance requirements are fewer compared to private limited companies.

LLP continues regardless of death, retirement, or change.

Partners can decide internal management policies without rigid formalities.

Existing firms can easily convert into an LLP structure.

The eligibility criteria to form a Limited Liability Partnership (LLP) typically include the following points:

Minimum of 2 partners required, with at least one resident in India.

No maximum limit on the number of partners.

Partners must be above 18 years and legally capable of contracting.

A registered office address is mandatory.

Partners must have valid identity and address proofs.

Here’s a checklist for forming a Limited Liability Partnership (LLP):

Decide LLP name and ensure availability on MCA portal.

Obtain Digital Signature Certificate (DSC) for all partners.

Apply for Director Identification Number (DIN) of designated partners.

Draft and file incorporation documents with ROC.

Execute and file LLP Agreement within 30 days.

Apply for PAN, TAN, and GST (if applicable).

Open a current bank account in LLP name.

Here’s a checklist for forming a Limited Liability Partnership (LLP):

Decide LLP name and ensure availability on MCA portal.

Obtain Digital Signature Certificate (DSC) for all partners.

Apply for Director Identification Number (DIN) of designated partners.

Draft and file incorporation documents with ROC.

Execute and file LLP Agreement within 30 days.

Apply for PAN, TAN, and GST (if applicable).

Open a current bank account in LLP name.

The following necessary documents are crucial for Limited Liability Patnership in India:

Decide LLP name and ensure availability on MCA portal.

Obtain Digital Signature Certificate (DSC) for all partners.

Apply for Director Identification Number (DIN) of designated partners.

Draft and file incorporation documents with ROC.

Execute and file LLP Agreement within 30 days.

Apply for PAN, TAN, and GST (if applicable).

Open a current bank account in LLP name.

There are several types of LLPs based on the structure and purpose, though the basic framework remains the same. Here are some variations:

The most common type, where all partners manage the business and share profits, while enjoying limited liability protection.

Specifically designed for professional service providers like lawyers, accountants, architects, or consultants. In some regions, certain professions can only form LLPs under this category.

his structure is used for family-run businesses where all partners are members of the same family, combining business flexibility with limited liability.

In some cases, LLPs can involve partners from different professions (e.g., lawyers, accountants, and consultants). Each partner brings a unique skill set, and the LLP structure allows collaboration without joint liability.

Some jurisdictions allow LLPs to operate as non-profit entities, where the purpose is to serve a charitable or public good. Partners still benefit from limited liability, but the entity is structured to reinvest profits into the cause rather than distributing them to partners.

An LLP registered in one country but operating in another. Many businesses with international operations may use this structure to protect their interests across borders.

A Limited Liability Partnership (LLP) combines elements of both partnerships and corporations, offering a unique blend of flexibility and protection. Here are the key characteristics of an LLP:

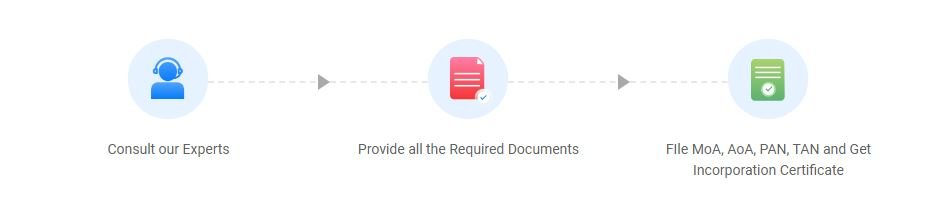

Registering a Limited Liability Partnership (LLP) involves several steps that may vary slightly depending on the jurisdiction, but the general process is fairly standard. Here’s a step-by-step guide on how to register an LLP:

To register an LLP, first decide on a unique name and ensure its availability on the MCA portal. Next, obtain Digital Signature Certificates (DSC) for partners and apply for Director Identification Numbers (DIN). File incorporation documents along with details of designated partners to the Registrar of Companies (ROC). Draft and execute the LLP Agreement within 30 days of incorporation, defining the rights and duties of partners. Once the incorporation certificate is issued, apply for PAN, TAN, and GST if applicable. Finally, open a current account in the LLP’s name to begin operations legally.

At least 2 partners are required, with no maximum limit.

Yes, to legally operate as an LLP, registration is required.

Yes, LLPs can raise funds but not through equity shares.

LLPs must file annual returns and statements of accounts.

Yes, LLPs can be converted into a Private Limited Company.

At ADTAXS, we are committed to providing expert consulting services to help your business succeed. Our specialties include comprehensive tax solutions, legal advisory, and essential business registration.

By continuing past this page, you agree to our Terms and conditions , Cookie Policy, Privacy Policy and Refund Policy © – DAV Business Services Pvt. Ltd. All rights reserved.

Copyright © 2010-2024, All Right Reserved DAV Business Services Pvt. Ltd.