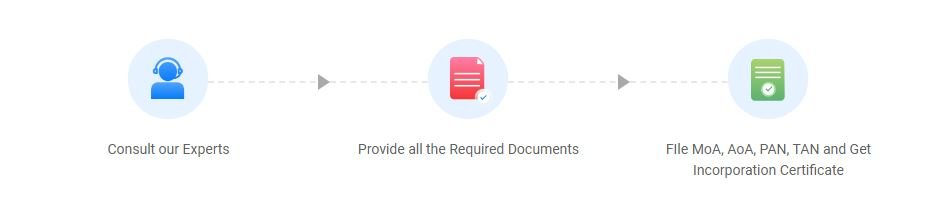

Get free Consultant With out Experts.

Notice: File your Company Audit before the 30th September deadline. Talk to our expert

India’s highest-rated

legal tax and compliance platform.

Vakilsearch’s incorporation experts register over 1500 companies every month.

Talk to our experts to kickstart your business registration process.

The Companies Act, 2013 in India requires companies to maintain accurate financial records, including bank reconciliations, that reflect their true financial condition

Bank reconciliation is the process of comparing a company’s internal financial records (cash book) with the bank statement to ensure both match. This helps identify discrepancies such as errors, unrecorded transactions, or missing entries. The goal is to verify that the bank balance matches the company’s accounting records and resolve any differences. Regular bank reconciliation ensures accuracy in financial reporting and helps detect fraudulent activity or accounting mistakes. It is an essential practice for maintaining reliable financial records and accurate cash flow management.

Bank reconciliation is the process of matching the entries in a company’s accounting records (like cash books) with the bank’s records (bank statements). It helps identify any discrepancies between the two, such as errors in recording transactions, unprocessed checks, or deposits not yet reflected by the bank. This process is crucial for ensuring accurate financial reporting, verifying that all transactions have been accounted for, and maintaining reliable cash flow. Regular bank reconciliation helps businesses avoid errors, detect fraud, and ensure compliance with financial regulations.

Bank reconciliation helps ensure that the company’s financial records are accurate by comparing them to the bank's records. This reduces errors and discrepancies in financial reporting.

Regular reconciliation can help identify fraudulent activities or unauthorized transactions early, allowing businesses to take corrective action promptly.

It helps in identifying errors such as double entries, missing transactions, or bank charges that may have been overlooked, allowing for timely corrections.

Regular reconciliation provides a clear, accurate, and updated view of financial data, improving transparency and making it easier for businesses to prepare for audits.

Automation of invoice generation, payment reminders, and transaction tracking streamlines processes, saving time and reducing human error.

Accurate reconciliation helps businesses maintain proper financial records, ensuring compliance with regulatory requirements and protecting them from potential legal issues or penalties.

Valid Business Operations:

Access to Bank Statements:

Accurate Internal Records:

Accounting Software (Optional):

Knowledge or Expertise in Accounting:

Timely Reconciliation:

Gather Bank Statements:

Verify Opening Balance:

Match Deposits:

Verify Withdrawals/Payments:

Identify Unprocessed Transactions:

Reconcile Bank Charges:

Check for Errors:

Adjust for Timing Differences:

Correct Discrepancies:

Confirm Reconciliation:

Document Reconciliation:

Bank Statements:

Cash Book or General Ledger:

Check Register:

Deposit Slips/Receipts:

Bank Fees and Charges:

Transaction Receipts/Invoices:

Unprocessed Checks or Pending Transactions:

Accounting Software (Optional):

This is the most common type, where businesses reconcile their bank account with their internal records on a monthly basis, typically at the end of each month. It ensures that the records align with the bank statement for that period.

Some businesses prefer to perform bank reconciliation every three months. This type is useful for businesses that have fewer transactions or when monthly reconciliation is not necessary. However, it may not catch discrepancies as quickly as monthly reconciliation.

This is performed once a year, often at the end of the fiscal year, to prepare for tax filing and auditing. While less frequent, it may be suitable for small businesses or those with minimal transaction volume.

Accuracy:

Timeliness:

Detailed Comparison:

Identifies Discrepancies:

Adjustments and Corrections:

Prevents Fraud:

Enhances Cash Flow Management:

Auditing and Compliance:

Open a Bank Account for the Business

2. Set Up Accounting Software or System

3. Get Access to Your Bank Statements

4. Record All Transactions in Your Internal System

5. Perform Regular Reconciliation

6. Make Adjustments

7. Maintain Supporting Documentation

8. Hire a Professional (Optional)

At ADTAXS, we are committed to providing expert consulting services to help your business succeed. Our specialties include comprehensive tax solutions, legal advisory, and essential business registration.

By continuing past this page, you agree to our Terms and conditions , Cookie Policy, Privacy Policy and Refund Policy © – DAV Business Services Pvt. Ltd. All rights reserved.

Copyright © 2010-2024, All Right Reserved DAV Business Services Pvt. Ltd.