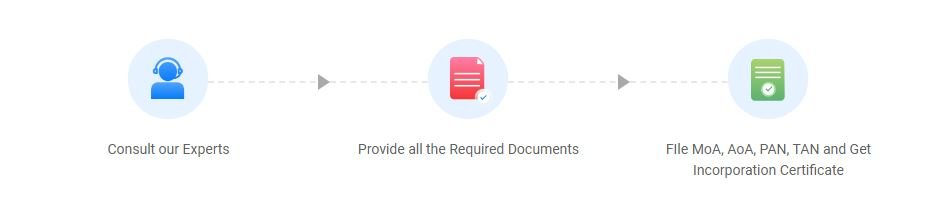

Get free Consultant With out Experts.

Notice: File your Company Audit before the 30th September deadline. Talk to our expert

India’s highest-rated

legal tax and compliance platform.

Vakilsearch’s incorporation experts register over 1500 companies every month.

Talk to our experts to kickstart your business registration process.

Section 128(1) requires every company to prepare and keep the books of account and other relevant books and papers and financial statements at its registered office.

Bookkeeping is the process of recording, organizing, and maintaining a company’s financial transactions systematically. It involves documenting every financial activity, such as sales, purchases, payments, and receipts, to ensure accurate financial records.

Bookkeeping is the practice of systematically recording and maintaining a company’s financial transactions. It includes documenting all financial activities, such as sales, expenses, and payments, on a daily basis. The goal of bookkeeping is to ensure that all financial records are accurate and organized, providing a clear picture of a business’s financial health. Bookkeeping is essential for creating financial reports, tracking cash flow, and preparing for tax filing, ultimately helping businesses make informed financial decisions.

Bookkeeping helps track your business's income and expenses, providing a clear overview of your financial health and making it easier to manage cash flow.

Accurate bookkeeping ensures that your financial records are up-to-date, making it easier to file taxes on time and avoid penalties for non-compliance.

With organized financial records, business owners can make informed decisions based on real-time financial data and trends.

Proper bookkeeping helps identify unnecessary expenses and areas where costs can be reduced, leading to better profitability.

By understanding your financial position, bookkeeping allows for better budgeting, planning, and allocation of resources to support business expansion.

Organized and accurate financial records make audits simpler, faster, and less costly, reducing stress during audits or financial reviews.

Eligibility Criteria for Bookkeeping Services

Bookkeeping services are essential for all businesses, but the eligibility criteria for hiring or using professional bookkeeping services depend on several factors:

Business Type

Business Size

Income Level

Legal and Regulatory Requirements

Scope of Business Operations

Record-Keeping Standards

To ensure your bookkeeping is accurate and efficient, follow this checklist:

Business Information

Bank Statements

Income and Revenue Tracking

Expense Documentation

Invoice Management

Payroll Records

Tax Records

Accounts Receivable & Payable

Financial Reports

Software/Tools

Backup and Security

Audit and Review

To maintain accurate and efficient bookkeeping, the following documents are essential:

Receipts and Invoices

Bank Statements

Payment Records

Payroll Records

Tax Returns

Accounts Receivable and Payable

Purchase Orders and Bills

General Ledger

Business Agreements and Contracts

Loan Documents

Fixed Asset Records

Expense Claims

In India, private limited businesses are differentiated into different types based on share distribution and other aspects. Here are 3 different types of PVT ltd Companies:

This is the simplest form of bookkeeping, where each financial transaction is recorded once (either as an income or expense). It is mainly used by small businesses with straightforward financial activities.

This method records each transaction twice: once as a debit and once as a credit. It provides a more comprehensive view of the business's financial situation and ensures that the accounting equation (Assets = Liabilities + Equity) always balances.

This method uses accounting software (such as QuickBooks, Xero, or Zoho Books) to track financial transactions automatically. It helps streamline and automate the process, reducing human errors and improving efficiency for businesses of all sizes.

Systematic Recording

Accuracy

Consistency

Transparency

Regulatory Compliance

Financial Analysis

Timeliness

Supports Auditing

Cost-Effective

Helps in Tax Filing

Determine Your Business Needs

Select the Type of Bookkeeping

Choose Bookkeeping Software or Service

Register with a Service Provider (if hiring a professional)

Prepare Necessary Documents

Set Up Your Financial Systems

Ongoing Recordkeeping

There are several criteria that determine the total fees structure to form a private limited business in India. Fees like stamp duty and government fees are required. Professional fees will be assessed if you engage any experts. Apart from this, applications for filing DSC, DIN, Notary fees, PAN, TAN and GST registration should be accounted for. An all-in-one platform for online private limited company registration in India is offered by Vakilsearch. Depending on your demands, you can choose from our affordably priced packages and begin the registration process.

At ADTAXS, we are committed to providing expert consulting services to help your business succeed. Our specialties include comprehensive tax solutions, legal advisory, and essential business registration.

By continuing past this page, you agree to our Terms and conditions , Cookie Policy, Privacy Policy and Refund Policy © – DAV Business Services Pvt. Ltd. All rights reserved.

Copyright © 2010-2024, All Right Reserved DAV Business Services Pvt. Ltd.