Get free Consultant With out Experts.

Notice: File your Company Audit before the 30th September deadline. Talk to our expert

Guaranteed IEC Code approval within 7 working days. 100% online process.

India’s highest-rated

legal tax and compliance platform.

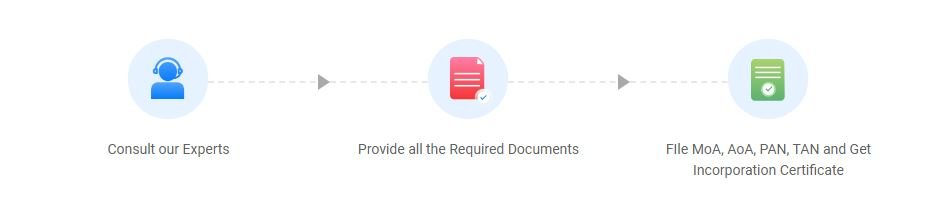

Talk to our experts to kickstart your business registration process.

Established the Export-Import Bank of India (EXIM Bank) to manage export credit. EXIM Bank provides products and services to support industries and small and medium-sized enterprises (SMEs).

The import-export business is a vital component of the global economy, facilitating the exchange of goods and services between countries and enabling businesses to expand their market reach. By importing goods, companies can offer a wider variety of products to consumers, often at lower prices due to favorable production costs in other countries. Conversely, exporting allows businesses to tap into new revenue streams and reduce dependence on local markets. This sector encompasses various industries, including agriculture, manufacturing, electronics, textiles, and more.

To succeed in the import-export business, companies must develop a comprehensive strategy that includes market research, identifying potential suppliers or buyers, and understanding the specific needs of different markets. Logistics plays a crucial role, as businesses must manage the complexities of transportation, customs clearance, and warehousing. Compliance with international trade laws, tariffs, and regulations is essential to avoid penalties and ensure smooth operations.

Import-export businesses can tap into international markets, allowing them to reach a broader customer base and increase sales potential beyond local boundaries.

By importing goods, companies can provide a wider variety of products to consumers, catering to diverse tastes and preferences that may not be met by domestic suppliers.

Importing goods from countries with lower production costs can lead to significant savings, allowing businesses to offer competitive pricing while maintaining healthy profit margins.

Engaging in international trade allows businesses to spread their risk across multiple markets, reducing reliance on a single domestic market and minimizing the impact of local economic downturns.

Exporting can lead to higher profit margins, especially if businesses offer unique products or services that are in demand in foreign markets.

Companies that successfully engage in international trade often enhance their brand reputation, demonstrating credibility and reliability to both domestic and international customers.

Eligibility Criteria for Import-Export Business

Import-Export Business Eligibility Checklist

Legal Registration

Tax Identification

Export/Import License

Compliance with Regulations

Financial Stability

Documents Required for Import-Export Business

Business Registration Documents

Tax Identification

Import/Export Licenses

Commercial Invoice

Packing List

Types of Import-Export Businesses

Businesses sell their products directly to foreign buyers without intermediaries. This approach allows for better control over pricing and customer relationships.

Involves selling products to intermediaries, such as export agents or trading companies, who then handle the sale to foreign markets. This method is often less risky and requires less expertise in international trade.

Businesses import goods from foreign manufacturers and sell them in their domestic market. This can include retail stores, wholesalers, or online platforms.

Businesses sell their products directly to foreign buyers without intermediaries. This approach allows for better control over pricing and customer relationships.

A reciprocal trading agreement where goods are exchanged for other goods instead of currency. This type of trade is often used in countries with limited access to foreign currency.

Collaborations between local and foreign companies to share resources and market entry strategies. This type can enhance market penetration and reduce risks associated with international trade.

Characteristics of Import-Export Business

How to Register an Import-Export Business

Choose a Business Structure:

Select a Business Name:

Register the Business:

Obtain Necessary Licenses:

Get a Tax Identification Number:

Open a Business Bank Account:

Register for VAT/GST (if applicable):

Compliance with Local Regulations:

Develop a Business Plan:

Consult Professionals:

Join Trade Associations:

Yes, IEC is required for customs clearance and foreign trade transactions.

Usually within 7 working days of online application.

Yes, even a sole proprietor can apply for IEC.

Export incentives under MEIS, SEIS, and reduced customs duties.

Yes, GST registration is mandatory if turnover exceeds the threshold.

At ADTAXS, we are committed to providing expert consulting services to help your business succeed. Our specialties include comprehensive tax solutions, legal advisory, and essential business registration.

By continuing past this page, you agree to our Terms and conditions , Cookie Policy, Privacy Policy and Refund Policy © – DAV Business Services Pvt. Ltd. All rights reserved.

Copyright © 2010-2024, All Right Reserved DAV Business Services Pvt. Ltd.