Get free Consultant With out Experts.

Notice: File your Company Audit before the 30th September deadline. Talk to our expert

India’s highest-rated

legal tax and compliance platform.

Vakilsearch’s incorporation experts register over 1500 companies every month.

Talk to our experts to kickstart your business registration process.

The Companies Act, 2013 in India primarily governs the registration and regulation of companies. However, it does not directly apply to partnership firms. Partnership firms are instead governed by the Indian Partnership Act, 1932, which defines the rules, responsibilities, and obligations of the partners.

A Partnership Firm is a business structure where two or more individuals agree to operate a business together and share profits. Partners are jointly responsible for managing the business, bearing risks, and fulfilling obligations. The terms of the partnership, such as profit-sharing ratios and duties, are clearly outlined in a Partnership Deed.

A partnership firm is a type of business organization in which two or more individuals come together to conduct business with the goal of making a profit. Partnerships are built on mutual consent and cooperation, and they play a significant role in the economy by facilitating various industries, from small businesses to larger enterprises.

Partnership firms require minimal paperwork and setup is quick.

Business responsibilities are shared, reducing stress on individual partners.

Partners combine expertise, skills, and funds to grow business faster.

Registration is inexpensive, making partnerships budget-friendly for small businesses.

Partners can manage operations freely without strict compliance burdens.

Profits are divided fairly among partners based on partnership deed.

To form a Partnership Firm in India, the following requirements must be met:

Minimum of 2 partners (maximum 20 allowed)

Partners must be Indian citizens and above 18 years of age

A valid Partnership Deed signed by all partners

Registered office address for the firm

Partners must be legally capable of entering into contracts

Here’s a simple checklist to help you set up you Partnership Firm

in India:

Decide the business name

Draft a Partnership Deed with profit-sharing details

Collect KYC documents of all partners

Obtain proof of business address

Apply for PAN Card of the firm

Open a current account in the firm’s name

Apply for GST / Shops & Establishment License if required

Here’s a list of documents required to register a Partnership Firm The exact requirements may vary by country or region, but generally, the following documents are commonly needed:

PAN Card of all partners

Aadhaar Card or valid ID/address proof of partners

Passport-size photos of all partners

Registered office proof (rent agreement/utility bill)

Partnership Deed signed by all partners

PAN Card of the firm

Bank account details in the firm’s name

GST registration (if applicable)

A sole proprietorship typically refers to a single-owner business, but there are various types or forms it can take, depending on the nature of the business and the owner’s preferences. Here are some common types of sole proprietorships:

A partnership firm officially registered under the Indian Partnership Act, 1932. It enjoys legal protection and the right to sue third parties in case of disputes.

A partnership firm not registered under the Act. It is valid and legal, but partners cannot sue each other or third parties in court for settlement of disputes.

Though governed separately under the LLP Act, 2008, this structure combines partnership flexibility with limited liability protection, making it a preferred option for many businesses.

A Partnership Firm is flexible, simple, and resource-efficient, making it an excellent choice for small businesses with multiple owners.

Formed by two or more individuals (maximum 20 partners)

Governed by the Indian Partnership Act, 1932

Partnership Deed defines profit-sharing and responsibilities

Partners have unlimited liability

Not a separate legal entity (partners and firm are the same in law)

Dissolves automatically upon death or withdrawal of a partner unless otherwise agreed

Easy to convert into LLP or Private Limited Company if business grows

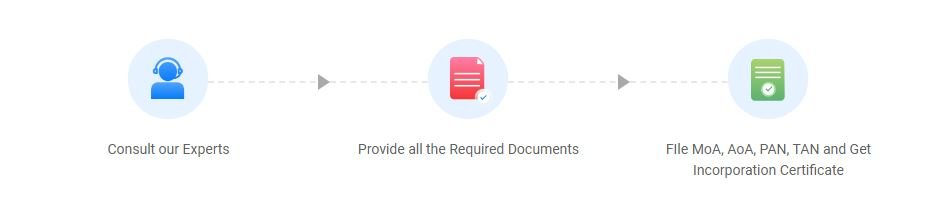

To register a Partnership Firm, begin by choosing a business name and drafting a Partnership Deed that defines roles, duties, and profit-sharing among partners. Collect KYC documents and proof of the business address. Apply for a PAN card in the firm’s name and open a current bank account for business operations. Depending on your business, you may need GST registration, Shops & Establishment license, or MSME registration. Registration under the Indian Partnership Act, 1932 is optional but recommended, as it provides legal recognition and better protection in case of disputes.

A partnership firm is an effective business structure that offers many advantages, such as shared responsibilities, access to capital, and flexibility in management. However, it also comes with certain risks, particularly concerning unlimited liability in general partnerships. Understanding the various types, characteristics, and the registration process is crucial for individuals considering forming a partnership. This knowledge can help in making informed decisions that align with the business goals and personal preferences of the partners involved.

No, registration is optional. However, registered firms enjoy better legal protection and rights.

At least 2 partners are required, and a maximum of 20 are allowed.

A Partnership Deed is a written agreement that outlines the terms of partnership, including roles, duties, and profit-sharing ratios.

Partnership Firms are taxed at a flat rate of 30% plus applicable surcharge and cess.

Yes, Partnership Firms can be converted into an LLP or Private Limited Company when the business expands.

At ADTAXS, we are committed to providing expert consulting services to help your business succeed. Our specialties include comprehensive tax solutions, legal advisory, and essential business registration.

By continuing past this page, you agree to our Terms and conditions , Cookie Policy, Privacy Policy and Refund Policy © – DAV Business Services Pvt. Ltd. All rights reserved.

Copyright © 2010-2024, All Right Reserved DAV Business Services Pvt. Ltd.